Both are digital dollars. Both settle fast. The differences are more important than the similarities.

There's a quiet debate underway in institutional finance that your leadership team is about to be forced to have an opinion on: tokenized deposits versus stablecoins as the preferred on-chain dollar for enterprise payments.

Analysts are predicting tokenized deposits could overtake stablecoins for institutional and wholesale use in 2026. Before that debate lands on your desk, here's the map.

Start with what they have in common

Both are digital representations of U.S. dollars that can move on blockchain rails, settle near-instantly, and operate outside traditional banking hours. From an end-user payments perspective, they're functionally similar: send value, receive value, settle fast, pay very little.

What a stablecoin actually is

A stablecoin is issued by a licensed entity — Circle for USDC, Tether for USDT — that holds reserve assets backing each token 1:1. Under the GENIUS Act, those reserves must be high-quality liquid assets, attested monthly.

The key property: stablecoins are portable. USDC moves across Ethereum, Solana, Stellar, and dozens of other networks. It can be held in any compatible wallet, used in any application that accepts it, and transferred to any counterparty without requiring either party to have a relationship with the issuer. No pre-existing banking relationship required.

What a tokenized deposit is

A tokenized deposit is a digital representation of a commercial bank deposit, issued on a blockchain by the bank itself. Your $1 million deposit at JPMorgan becomes a token that can move on-chain — but it's still a JPMorgan deposit. It carries deposit insurance up to applicable limits. It can potentially earn a yield. It stays within the bank's regulated environment.

The key property: tokenized deposits carry institutional familiarity. They look and behave like money your team already manages, just on faster rails.

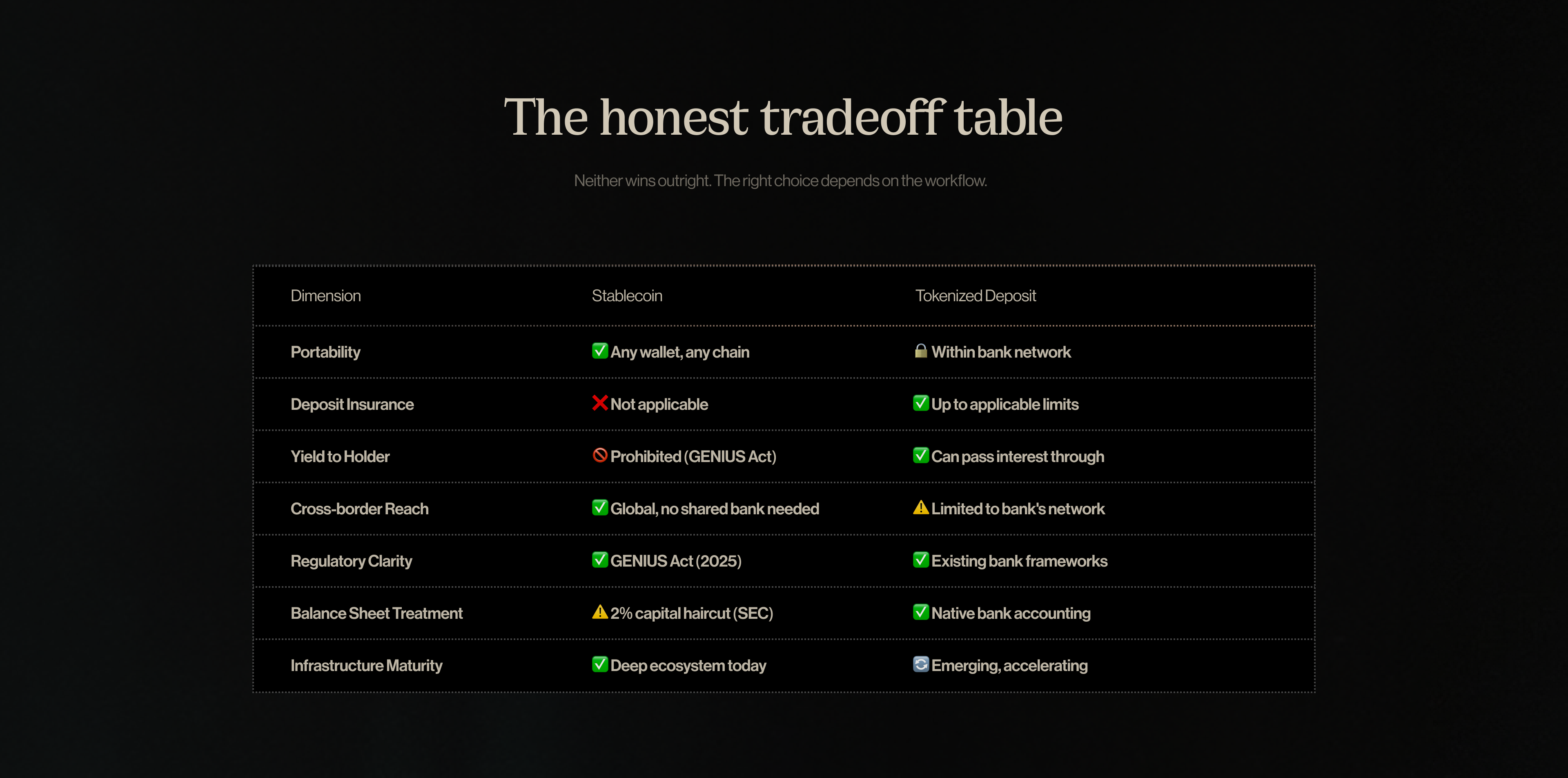

The tradeoffs, honestly

Stablecoins win on portability and interoperability. Any counterparty with a wallet can receive USDC — no shared banking relationship required. That's decisive for cross-border payments to counterparties outside your bank's network, mass payouts to contractors globally, or settlement with partners in markets where your bank has thin coverage.

Tokenized deposits win on regulatory clarity and balance-sheet treatment. They sit within existing bank supervision frameworks. The SEC's recent 2% capital haircut guidance applies to qualifying payment stablecoins — but deposit insurance and bank-grade custody are native to tokenized deposits in a way they aren't yet to stablecoins.

The yield question is also real. Stablecoins, under the GENIUS Act, cannot offer yield directly to holders — that provision exists to prevent them from functioning as unregulated bank deposits. Tokenized deposits can, in principle, pass interest through. For teams managing large idle balances, that's not a trivial difference.

What this means practically

The honest answer is: both will coexist, and the choice depends on your use case.

For domestic, institutional settlement between entities that share banking relationships, tokenized deposits may win on familiarity and compliance simplicity.

For cross-border payments, mass payouts, emerging market corridors, and transactions with counterparties outside your banking network, stablecoins currently have the infrastructure advantage.

The better question isn't "which one should we use?" It's: which of our payment workflows would benefit from faster settlement, and then figure out which digital dollar fits each one.

Fin helps businesses move money across borders using stablecoin rails without the complexity. Explore fin.com →