Three sentences in an FAQ changed the balance-sheet math for every broker-dealer holding stablecoins. Here's the translation.

On February 19, 2026, the SEC's Division of Trading and Markets added Question No. 5 to its Broker-Dealer Financial Responsibility FAQ. No press release. No rulemaking. Just a few lines that moved stablecoins from "balance sheet liability" to "working capital" for regulated financial institutions.

First: what a capital haircut actually is

When a broker-dealer calculates its net capital — the cushion it holds against obligations — it applies discounts ("haircuts") to the assets it's counting. The riskier or less liquid the asset, the steeper the haircut. A 100% haircut means the asset counts for nothing in your capital math. A 0% haircut means it counts at full face value.

Until last week, stablecoins had no explicit treatment. Many broker-dealers, out of caution, were applying a 100% haircut — meaning they needed to hold $2 million in other assets just to hold $1 million in stablecoins without impacting their capital ratios. In practice, this made stablecoin holdings a financial penalty.

What the guidance says

Broker-dealers can now apply a 2% haircut to qualifying payment stablecoin positions. That means $1 million in USDC allows $980,000 to count toward net capital.

Commissioner Hester Peirce's accompanying statement explained the logic plainly: a 2% haircut aligns with how registered money market funds are treated — vehicles that hold the same types of instruments (short-term Treasuries, cash, government securities) that back qualifying stablecoins. Treating a stablecoin like a speculative token was, in her words, "unnecessarily punitive."

Not all stablecoins qualify

The guidance applies to a defined category of "payment stablecoins" — and the definition is specific. Currently, qualifying stablecoins must be issued by a state-regulated money transmitter, trust company, or national trust bank, backed by GENIUS Act-standard reserves, with a public redemption policy and monthly attestation from a registered accounting firm. After GENIUS Act regulations take full effect, the definition transitions to any stablecoin issued by a "permitted payment stablecoin issuer" under that legislation.

USDC likely qualifies. Many others may not. This guidance has just created a concrete compliance filter for institutions evaluating which stablecoins to hold.

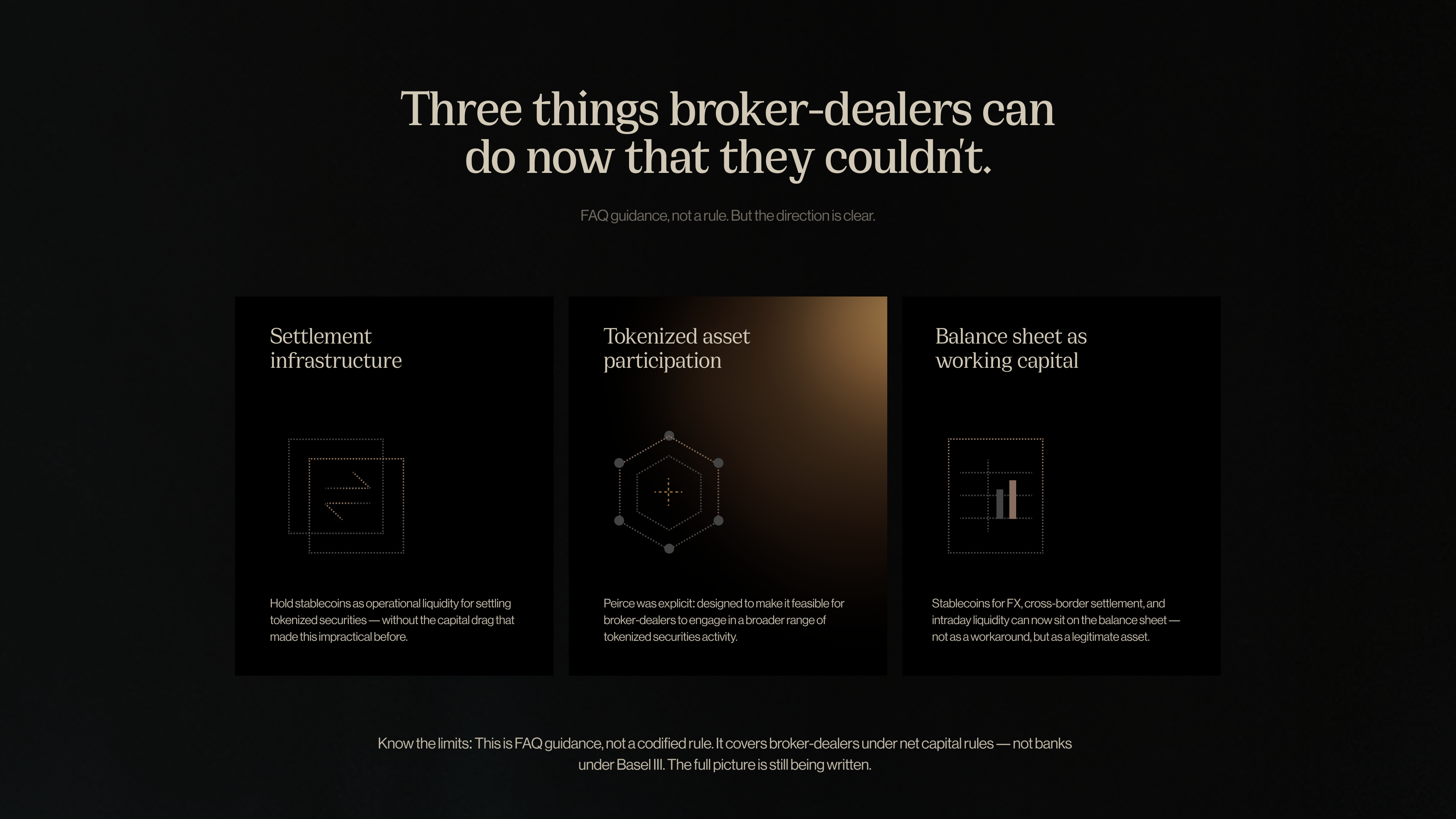

What it unlocks

Three things change immediately for broker-dealers:

Settlement infrastructure. Stablecoins can now be held as operational liquidity for settling tokenized securities — without the capital drag that previously made this impractical.

Tokenized asset participation. Commissioner Peirce was explicit: this guidance is designed to make it "feasible for broker-dealers to engage in a broader range of business activities relating to tokenized securities." The firms sitting on the sidelines of tokenized asset markets have one fewer reason to stay there.

Balance sheet management. For firms moving large dollar amounts on blockchain rails — FX, cross-border settlement, intraday liquidity — stablecoins can now function as working capital rather than an off-balance-sheet workaround.

The honest limits

This is FAQ guidance, not a rule. The current SEC leadership's view, not a formal regulation. Peirce herself noted she'd "like to consider how Rule 15c3-1 could be amended" to codify this treatment permanently — a hint that legislative backing is needed for durability.

It also applies to broker-dealers specifically, under their net capital rule. Banks operating under Basel III and Fed capital frameworks are governed separately. The full banking-system picture on stablecoin capital treatment is still being written.

The direction is clear. "Regulated stablecoin" is now a meaningful distinction — and institutions moving toward GENIUS Act-compliant instruments are positioning themselves ahead of a framework that is firming up fast.

Fin helps institutions and enterprises move value on stablecoin rails — compliantly, and without the complexity. fin.com →