There's a specific kind of financial anxiety that doesn't get enough airtime in fintech conferences: waking up in a country where your savings lost 40% of their value last year — not because of anything you did, but because of where you were born.

Nsave was built for exactly that person. Their product gives people in high-inflation, currency-unstable markets — particularly across South Asia and the broader diaspora — the ability to hold and move money globally. They offer local currency accounts and global money movement for users who are often underserved by both traditional banking and the first generation of fintech apps that forgot entire continents existed.

The corridors they serve — India, the Philippines, Pakistan — carry their own compliance complexity, their own FX dynamics, and their own banking access constraints. Building across all of them simultaneously requires infrastructure that can hold that complexity without passing it upstream to the product team or downstream to the customer.

That's where Fin comes in.

What Fin builds for Nsave

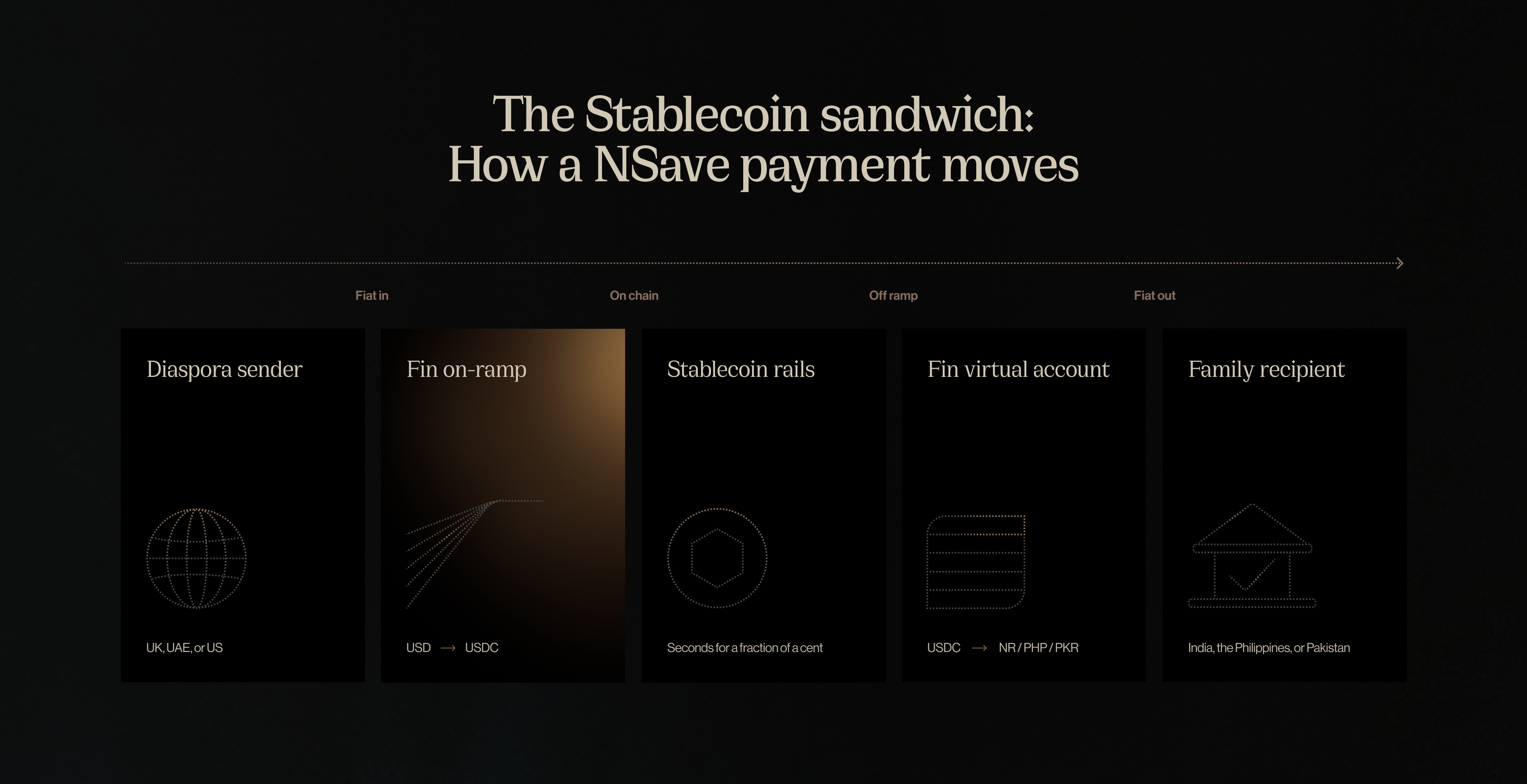

Fin provides the settlement and virtual account infrastructure that makes Nsave's cross-border product work at the rails level.

INR, PHP, and PKR virtual accounts allow Nsave's users to receive funds in their home currency without navigating international wire mechanics themselves. A user in Manila receives Philippine Pesos into a local account. A family in Lahore receives Pakistani Rupees. The cross-border complexity is entirely invisible to them — which is exactly how it should be.

Alongside the virtual accounts, Fin provides local off-ramp connectivity in each corridor and a stablecoin settlement layer that handles the cross-border value transfer between send and receive. Rather than routing through a chain of correspondent banks — each adding time, cost, and a potential point of failure — value moves via stablecoin rails and arrives as local currency at the destination. Fast, low-cost, and auditable.

The KYB framework Fin provides sits underneath all of it. South Asia remittance flows attract compliance scrutiny by default. Getting the compliance infrastructure right at the rails level isn't optional — it's the precondition for everything else working, and for Nsave being able to operate confidently in corridors that less well-prepared providers avoid.

Why this matters

The South Asian diaspora sends over $200 billion home every year. A meaningful portion of that flows through remittance channels that charge 5–7% and take two to five days to settle. Nsave's product — and Fin's infrastructure underneath it — is aimed squarely at that gap.

Fin's role here isn't to replace banks in India or the Philippines. It's to extend dollar-denominated settlement reach into corridors where correspondent banking economics make it unviable at the price points real people can afford. The virtual accounts make receipt seamless. The stablecoin settlement layer makes the economics work. The KYB framework makes it compliant. Together, they make the product possible.