This isn't about Zuckerberg. It's about what happens to your internal approval process when 3.6 billion daily users are on the same rails you've been evaluating.

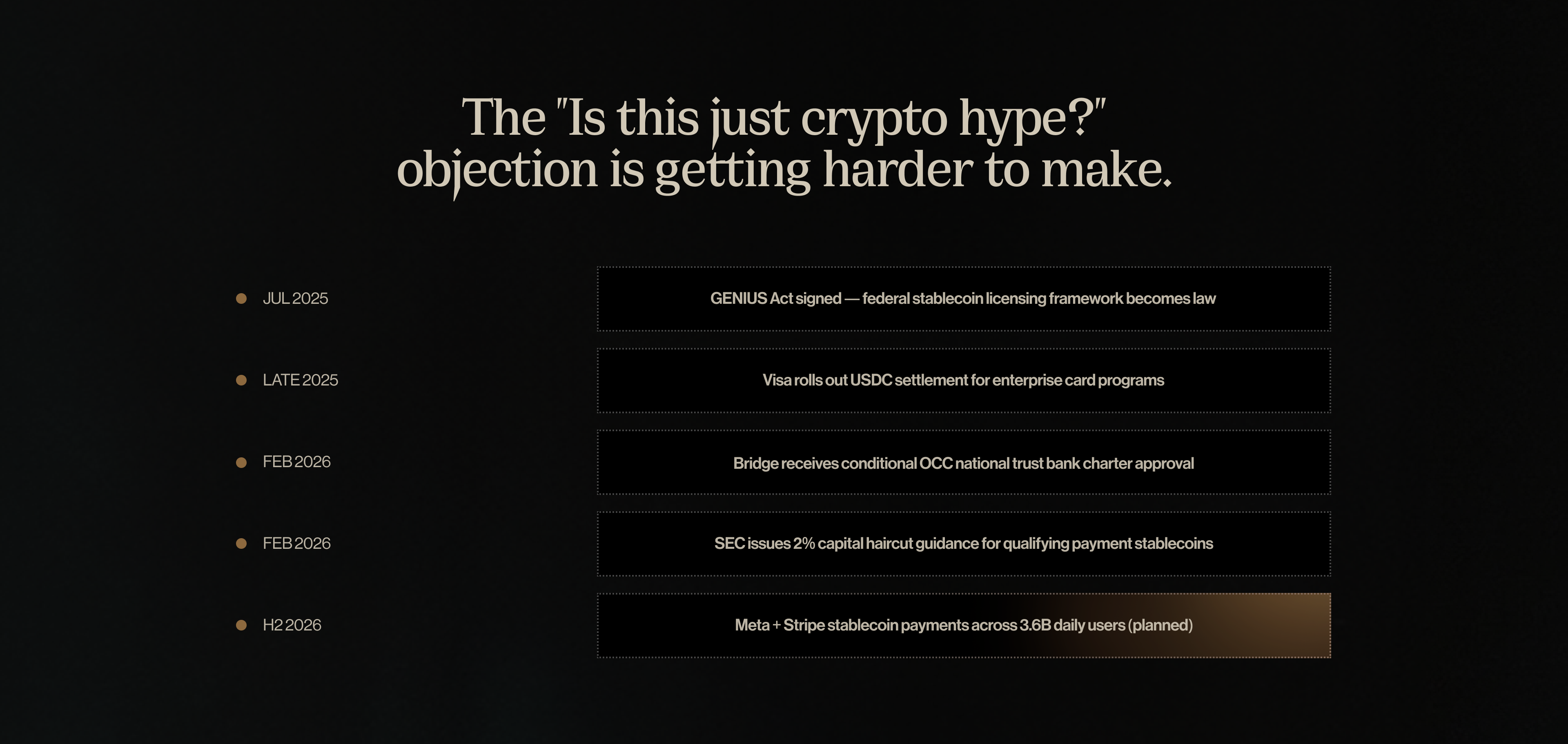

On February 24, 2026, CoinDesk reported that Meta is planning to integrate stablecoin payments across Facebook, Instagram, and WhatsApp in H2 2026 — likely through Stripe and its Bridge infrastructure. Meta's PR team immediately clarified there's no Meta stablecoin yet. True. But that's not an interesting story.

The interesting story is what it signals for businesses that have been slow-walking their stablecoin evaluation.

What Meta is actually doing (and not doing)

Meta is not issuing a stablecoin. Libra taught them that lesson the hard way: $182 million in sold assets and a shutdown wallet by 2022.

What they're doing is positioning as a distribution layer. They want to plug existing stablecoin rails (likely USDC via Bridge, Stripe's stablecoin infrastructure acquisition) into their apps, point their 3.6 billion daily active users at the on/off ramp, and let the payments flow — particularly for creator payouts and cross-border transfers where wire fees on small amounts are punishing.

The key quote from a source close to the plans: "They want to do this, but at arm's length." That's the right model — and it's the one most enterprise businesses should be thinking about too.

The Stripe angle matters more than the Meta headline

Stripe acquired Bridge for $1.1 billion in 2024. Bridge received conditional OCC approval for a national trust bank charter in February 2026. Stripe's 2025 annual letter noted Bridge's transaction volume quadrupled last year. Stripe CEO Patrick Collison sits on Meta's board.

This isn't a vendor relationship, it's a strategic infrastructure alignment between the company that processes a significant share of global internet commerce and the stablecoin infrastructure company with a federal bank charter pending.

When Stripe speaks, enterprise finance listens. When Stripe and Meta speak together, your board will ask why your company hasn't moved yet.

What does it actually change for your approval process?

Internal stablecoin adoption proposals inside large companies live or die on one question: "Is this real, or is this crypto hype?" The answer to that question has been getting harder to dismiss since the GENIUS Act, the SEC's capital haircut guidance, and Visa's USDC settlement rollout. Meta-via-Stripe pushes the answer further.

The practical effect is institutional credibility transfer. Your leadership may not follow stablecoin infrastructure news. They do follow what Meta and Stripe are doing with payments. When enterprise technology platforms at this scale adopt stablecoin rails for real commercial use cases — creator payouts and cross-border transfers — the conversation inside your company shifts from "should we look at this?" to "why haven't we?"

The questions worth asking now

If stablecoin settlement becomes the default for payments on platforms your business already uses — ad purchases, marketplace payouts, creator payments — are you operationally ready to receive and reconcile those payments?

If your largest counterparties start settling in USDC because their bank now offers it as a standard option (and FDIC applications are being filed right now), does your payment stack handle that today?

The Meta news won't change your payment operations next quarter. But it's another data point in a trend that has been moving in one direction for 18 months.

Fin is built for exactly this moment — helping businesses get onto stablecoin rails before the wave arrives, not after. fin.com →