Your bank might soon be a stablecoin issuer. Here's what that changes — and what it doesn't.

The stablecoin conversation in enterprise finance has been framed as "traditional finance vs. crypto rails" for long enough that an important development is getting overlooked: banks are becoming stablecoin issuers themselves.

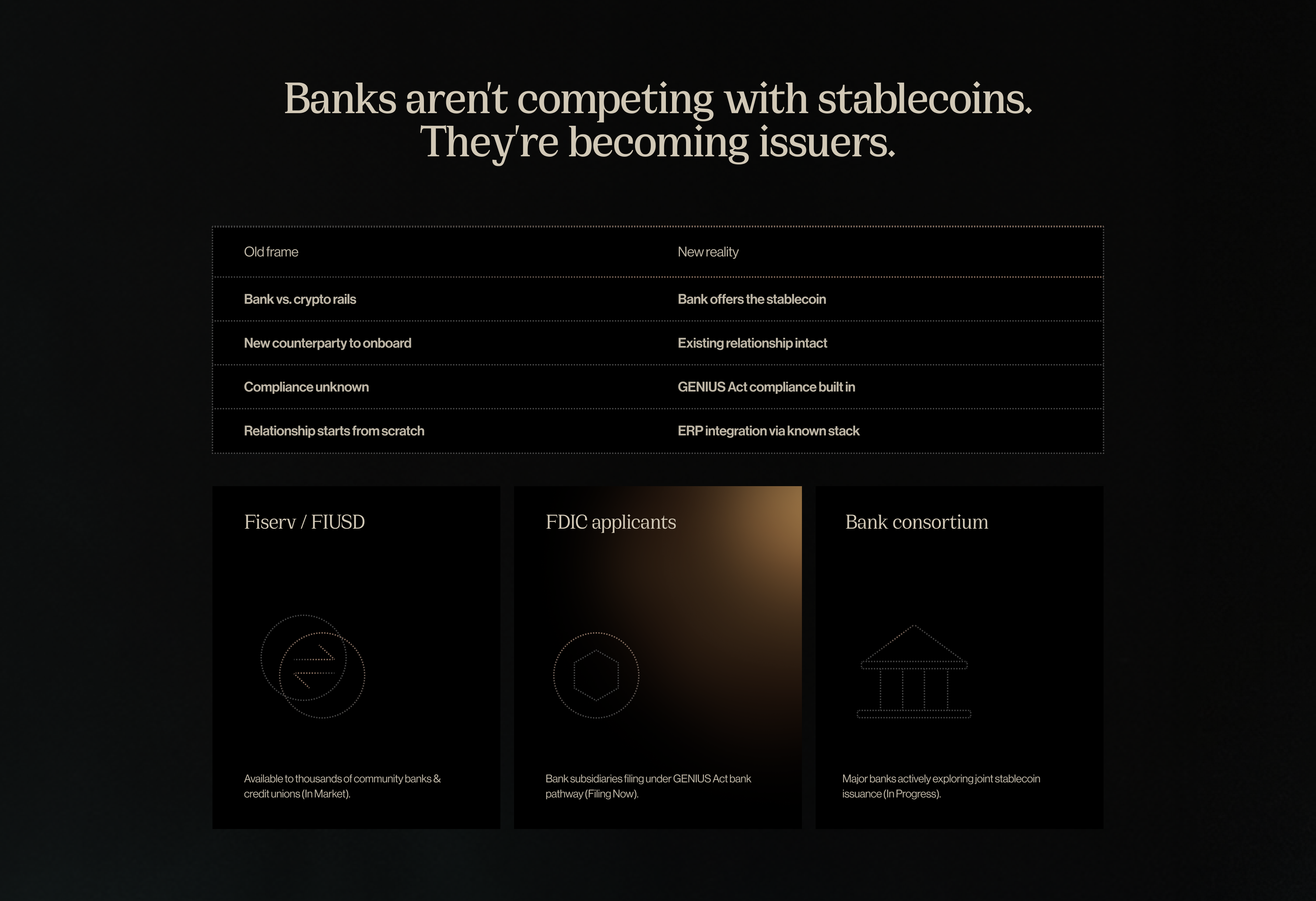

Fiserv has developed FIUSD. A consortium of major banks is actively exploring stablecoin issuance. The GENIUS Act's bank-subsidiary pathway has sparked FDIC applications. The frame of "crypto vs. traditional finance" was always wrong; it's just becoming more obviously wrong every month. At Fin, we've been arguing this since day one. The infrastructure isn't a replacement. It's an extension.

What bank-issued stablecoins actually are

A bank-issued stablecoin is, conceptually, a tokenized deposit — a digital representation of a bank liability that can move on blockchain rails. The bank issues the token, holds the reserves, and redeems it on demand. Existing depositors could potentially access faster, programmable, 24/7 payment capabilities through a product their bank already manages.

Fiserv's FIUSD is designed to be available to the thousands of community banks and credit unions that use Fiserv's core banking infrastructure. That's a potentially massive distribution reach for stablecoin access — not just for institutional clients, but eventually for retail customers.

How it changes the competitive landscape

Before bank-issued stablecoins, any business evaluating stablecoin adoption faced a choice between their existing bank (no stablecoin capability) and a crypto-native infrastructure provider (new compliance and counterparty considerations). That tradeoff was a meaningful barrier.

Bank-issued stablecoins collapse that choice. If your current banking partner offers a GENIUS Act-compliant stablecoin for settlement, the compliance and relationship considerations are already handled. The operational question becomes purely about capability and integration, not whether you need to onboard an entirely new counterparty.

The interoperability question is the hard one

Here's the issue that doesn't have a clean answer yet: will FIUSD and PYUSD and a JPMorgan-issued stablecoin and USDC all be interoperable? Can your counterparty receive FIUSD if you send it?

The answer today is: not necessarily, without infrastructure in between. The value of a stablecoin as a payment instrument depends on whether the recipient can accept and redeem it. A bank-issued stablecoin that only works within that bank's ecosystem is a faster ACH with extra steps, not a cross-border payment solution.

The protocols being built to solve these — cross-chain bridges, stablecoin DEXes, and interoperability standards — are real and maturing. It's also part of what Fin is working on: ensuring that whichever compliant stablecoin your counterparty uses, value can move between them cleanly. But interoperability between bank-issued stablecoins is an infrastructure problem that isn't fully solved yet, and anyone who tells you otherwise is selling something.

What it means for your strategy

If your primary banking partner issues a GENIUS Act-compliant stablecoin, your adoption path gets dramatically simpler. The compliance due diligence is reduced, the counterparty relationship exists, and the ERP integration may be easier because it happens within an existing banking technology stack.

Watch for which banks file FDIC applications in 2026. The ones who move fastest on GENIUS Act licensing will have a product to offer enterprise clients in 2027. That's relevant to your banking relationship conversations right now.

The broader point: stablecoins aren't something banks need to compete against. They're becoming something banks offer. The question isn't "do we work with our bank or use stablecoins?" It's increasingly "what stablecoin does our bank offer, and does it meet our use case requirements?" Fin sits in the middle of that answer — connecting whichever rails your bank and your counterparties end up on.